When I filed my first taxes, I thought are real estate taxes and property taxes the same. My accountant laughed and told me they weren’t. That moment taught me a lot. Many people use both terms like they mean one thing, but the IRS and your county assessor see them differently. In this guide, I’ll explain the difference in clear, simple words. You’ll learn what each tax means, what the IRS allows as a deduction, and how states like Montana and Minnesota handle them. Let’s make it easy so you know exactly what you’re paying—and what you can save.

What the IRS Says About Property vs Real Estate Taxes

The Internal Revenue Service (IRS) is the main authority that defines how both real estate taxes and property taxes are treated under U.S. law. When I first read the IRS rules, I was surprised at how specific they are. The IRS explains that property taxes fall into two types — real property (like your home or land) and personal property (like your car or boat). Under Treasury Regulation §1.164-3, only taxes that are based on the value of the property, called ad valorem taxes, can be deducted on your Schedule A (Form 1040).

So, if you own a home, your real estate tax applies to the land and buildings attached to it. But if you pay taxes on a car or RV, that’s personal property tax. Both can count toward your federal deduction only if the amount you pay is tied to the item’s assessed value. If the tax is a flat local fee for services, like trash or sewer, it doesn’t qualify. In simple terms, the IRS sees real estate tax as one part of the larger property tax category—but it’s the value-based part that matters for your return.

✅ Get expert financial guidance for your tax needs with experienced Tax Services Orlando professionals. Contact

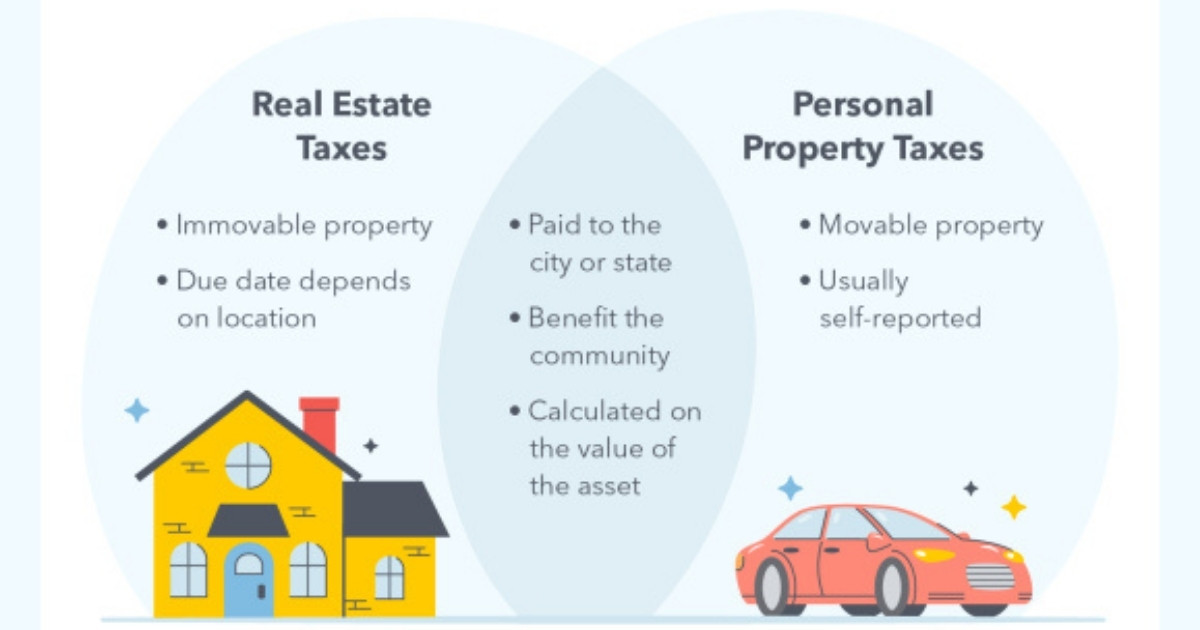

Real Estate Taxes vs Property Taxes — Detailed Comparison

I’ve paid both real estate taxes and property taxes, and they are not the same. Real estate taxes cover land and buildings. Property taxes include those plus things you can move, like cars or tools. The easiest way to remember this is simple — all real estate taxes are property taxes, but not all property taxes are real estate taxes. This small difference matters when you file taxes with the IRS.

Performance: Real Estate Taxes vs Property Taxes

Real estate taxes are based on your land and home. The County Assessor sets the value each year. The tax depends on that number. You can deduct the part based on value, called the ad valorem tax, on Schedule A (Form 1040). These taxes stay steady because they follow market value.

Property taxes include more things. They cover personal property, like vehicles and business gear. These items lose value faster, so your tax can change every year. Real estate taxes stay more stable, but property taxes change more from state to state, such as in Montana or Minnesota.

Ease of Use: Real Estate Taxes vs Property Taxes

Real estate taxes are easier to read. On your Property Tax Bill, you see the assessed value, the tax rate, and the ad valorem amount. It’s clear what you owe and what might count for a tax break. I like to check this once a year so I can plan my budget.

Property taxes can be harder. They often include non-ad valorem charges like trash, sewer, or fire service. These are not based on property value, so the IRS does not allow a deduction under Treasury Regulation §1.164-3. I once counted those by mistake and had to fix my return. Real estate taxes are simpler to follow. Property taxes need extra care.

Value for Money: Real Estate Taxes vs Property Taxes

Real estate taxes feel fair. They help pay for schools, parks, and roads. You see the results in your area. It feels like you are giving back to your community.

Property taxes on personal property, like a car or a boat, feel less helpful. You pay each year for something that keeps losing value. Real estate taxes build long-term worth. Property taxes often feel like a bill that comes with owning stuff.

Overall: Real Estate Taxes vs Property Taxes

Over the years, I’ve learned that real estate taxes are part of property taxes, but they matter more to homeowners. Property taxes cover both real and personal property, but only ad valorem taxes—those tied to value—count for IRS deductions. Real estate taxes are more stable, easier to understand, and often bring more lasting value.

Property taxes still matter because they fund local services, but they vary by what you own and where you live. Knowing the difference helps you pay the right amount, plan for the year, and avoid mistakes when filing. Always check the ad valorem part of your bill. That’s the part the IRS looks at when deciding what you can deduct.

| Category | Real Estate Taxes | Property Taxes |

| What It Covers | Land, homes, and buildings (anything fixed to the ground). | Both real property and movable items like cars, boats, or office tools. |

| Who Collects It | Usually the County Assessor or local government. | Local and state governments may both collect it. |

| How It’s Calculated | Based on the assessed value of land or buildings (ad valorem tax). | Based on the value of property you own — real or personal. |

| IRS Deduction Rule | Deductible under Schedule A (Form 1040) if it’s ad valorem. | Only the ad valorem portion is deductible; flat fees are not. |

| Example Items | Your house, garage, or land in states like Montana or Minnesota. | Your car, RV, boat, or business equipment. |

| Non-Deductible Fees | Local benefit charges (trash, sewer, fire) under Treasury Reg. §1.164-3. | Same rule — non-ad valorem service fees cannot be deducted. |

| Stability | Usually steady since it’s tied to property value. | Can change often if personal property value or laws shift. |

| Purpose | Supports public services — schools, roads, parks, and safety. | Funds both local services and general community needs. |

| Value for Money | Feels like an investment in your home and area. | Feels more like maintenance for owning movable items. |

| Best Tip | Always check the ad valorem section of your tax bill for IRS deductions. | Separate personal property and service fees before filing. |

Understanding Real Property and Personal Property

When I bought my first home, my county assessor sent me a tax notice filled with words I didn’t understand — real property and personal property. I asked my accountant, and he said the difference decides what type of tax I pay. Real property means things that stay in one place, like land and houses. Personal property means things you can move, like a car or a boat. The IRS and your county assessor treat these two very differently, and that affects your taxes each year.

Real Property — The Basis for Real Estate Tax

Real property covers land, homes, garages, and anything attached to the ground. If you can’t move it without breaking it, it’s real property. For example, your house in Montana, the garage, and the fence all count as real property. The County Assessor decides how much your land and home are worth, and that value is used to set your real estate tax.

The IRS lets you deduct these taxes on Schedule A (Form 1040), but only if they are ad valorem taxes — taxes based on property value. Real property taxes are steady and support schools, roads, and safety in your area. In short, real property is what your real estate tax covers, and it’s usually the most valuable thing you own.

Personal Property — The Broader Tax Base

Personal property means movable items like cars, RVs, boats, and business tools. States like Minnesota and Montana include these in property tax rules, but they use different systems.

If you pay a yearly tax based on your car’s value, that’s a personal property tax. If you pay a flat fee for registration, it’s not. The IRS, under Treasury Regulation §1.164-3, only allows deductions for value-based taxes. I learned this the hard way after trying to deduct my flat vehicle fee one year — it didn’t qualify.

If you run a business, these taxes matter even more. Your equipment loses value fast, which means your tax bill can drop each year. Real estate taxes stay steady, but personal property taxes change often.

The Ad Valorem vs Non-Ad Valorem Distinction

When I saw my first Property Tax Bill, I noticed two parts — ad valorem and non-ad valorem. I thought both were deductible, but I was wrong. The IRS only allows deductions for ad valorem taxes. That small detail can change your refund if you don’t notice it.

What “Ad Valorem” Means (and Why It Matters)

Ad valorem is a Latin term that means “based on value.” These taxes are tied to how much your property is worth. The IRS allows you to deduct ad valorem taxes because they depend on value, not a flat rate.

If your home is worth $300,000 and your local rate is 2%, your ad valorem tax is $6,000. You can list this on Schedule A (Form 1040) if you itemize. The key idea is simple — only value-based taxes are deductible under IRS rules.

What “Non-Ad Valorem” Covers (and Why It’s Not Deductible)

Non-ad valorem taxes are flat service fees. They pay for things like trash pickup, storm drains, fire service, and sewer systems. These help your neighborhood but don’t depend on your property’s value. That’s why the IRS says they can’t be deducted.

For example, a Montana or Sarasota County bill might list both. The ad valorem section is based on property value, while the non-ad valorem section lists fixed local fees. Only the ad valorem part is deductible. Mixing them up can lead to mistakes when you file.

Quick Example Table

| Type | Definition | Deductible? | Example |

| Ad Valorem | Based on property value | ✅ Yes | County real estate tax on a home or business building |

| Non-Ad Valorem | Fixed service fee | ❌ No | Sewer, trash, stormwater, or fire district fee |

Who Collects Property Taxes and How They’re Assessed

I learned fast that most bills come from the county. The county assessor sets value, and the county treasurer or tax office sends the bill. Cities and special districts can add their own lines. The short answer: counties lead the process, and others may add charges.

The state writes the rules, but locals do the work. State law defines classes, exemptions, and appeal steps. Your county applies those rules, sets local levies, and collects. The short answer: the state sets policy; the county sets and collects under that policy.

Your bill starts with assessed value. That number comes from sales data, cost models, or rent data for income property. Your tax is mostly assessed value × rate (ad valorem). The short answer: value times rate drives what you owe.

Bills often include two parts. One is ad valorem (value-based). The other is non-ad valorem (flat service fees like trash or stormwater). The short answer: only the value-based part affects deductions on Schedule A (Form 1040).

Montana keeps things county-driven under state rules. The assessor sets taxable value, and mills convert that to the bill. Personal property is often a business issue; many cars use fee systems outside ad valorem. The short answer: in Montana, counties assess and bill under a state frame, and value still leads.

Minnesota also runs through counties. The state uses property class and homestead rules that change how value turns into tax. Cities, schools, and districts add levies after hearings. The short answer: in Minnesota, class and homestead status shape how much you pay.

How does this hit your wallet? A higher assessed value or a higher levy raises the bill. A homestead or local exemption can lower it. Reading your property tax bill shows each driver in plain lines. The short answer: value up means tax up; exemptions and lower levies help.

If you mix up real estate taxes and property taxes, think scope. Real estate taxes hit land and buildings. Property taxes are the bigger bucket that can also include personal property. The short answer: all real estate taxes sit inside property taxes, but not all property taxes are real estate taxes.

State Examples — Montana and Minnesota

Montana Property Tax System

Montana runs on value first. The county assessor sets market value. The state turns that into taxable value. Mills then turn taxable value into your bill. The short answer: value × mills = what you owe.

Most lines on a Montana bill are ad valorem. That means they are based on value and can count on Schedule A (Form 1040). Flat service fees can appear too. Those are non-ad valorem and do not count. The short answer: value-based lines may be deductible; flat fees are not.

You may see exemptions or special rules. Rural land, farm gear, or small business items can get breaks under state law. Your county applies those rules to your parcel. The short answer: state rules set the breaks; your county applies them.

People often ask if real estate taxes vs property taxes are one and the same here. In practice, real estate taxes hit land and buildings. Property taxes can also include personal property for a business. The short answer: all real estate taxes are property taxes, but not all property taxes are real estate taxes in Montana.

How counties apply ad valorem rules (Montana)

Counties use sales and cost data to set value. They then apply the state’s class rules to get taxable value. Next, they apply county, city, and school mill levies. The short answer: value first, class next, mills last.

If a line is tied to value, it is ad valorem. If it is a flat charge for a service, it is not. Read your bill for the labels. The short answer: look for “ad valorem” on the bill to spot possible deductions.

Minnesota Property Tax Rules

Minnesota leans on classification. Homes, farms, and commercial sites each have their own class. Your homestead status can lower what you pay. The short answer: class and homestead shape the tax.

Minnesota also stacks levies. County, city, school, and special districts add their rates. All sit on top of your value. The short answer: many levies, one value base.

Folks search “are real estate taxes and property taxes the same Minnesota?” Day to day, people use both terms for the bill. For IRS rules, the split still matters. Real estate tax hits the house and land. Property tax can also include personal property in some cases. The short answer: same in casual talk, but not the same for tax rules.

Residential classification & exemptions (Minnesota)

A homestead home can get relief. Some local programs add credits or deferrals. Your county explains these on your property tax bill. The short answer: homestead and credits can lower the bill.

Minnesota also shows special assessments. These are non-ad valorem charges for local work, like sidewalks or storm drains. They do not depend on value and do not count as an IRS deduction. The short answer: special assessments are not value-based and are not deductible.

Property type variations (homestead vs commercial)

A homestead home and a commercial site can have very different class rules and rates. That changes how value turns into tax. Your line items will show who is taxing and why. The short answer: property type changes the math.

Whether you are in Montana or Minnesota, the steps are alike. Value comes first. Then class or taxable value. Then levies. Check each line to see if it is ad valorem or non-ad valorem before you claim a deduction. The short answer: value-based lines may be deductible; flat service fees are not.

Real-Life Filing Example (Schedule A Walkthrough)

I’ll use a simple case I see a lot. John owns a home and a car. His county bill shows two parts: ad valorem and non-ad valorem. He also paid a value-based car tax. Short answer: list value-based taxes, skip flat fees.

Step 1 — Read the bill.

John finds Ad Valorem Real Estate Tax = $1,214. He also sees Non-Ad Valorem Fees = $430 for trash and stormwater. The car line from the DMV shows Vehicle Tax (value-based) = $250. Short answer: mark $1,214 and $250 as value-based; treat $430 as a flat fee.

Step 2 — Match each item to IRS rules.

The IRS allows deductions for taxes based on value under Schedule A (Form 1040) and Treasury Reg. §1.164-3. That means the $1,214 and $250 can qualify. The $430 does not, since it is a flat service fee. Short answer: only ad valorem amounts qualify.

Step 3 — Enter the home amount.

On Schedule A, John enters $1,214 under state and local real estate taxes. He keeps the bill that shows the assessed value and the rate. This proves the tax is value-based. Short answer: put $1,214 on the real estate tax line.

Step 4 — Enter the vehicle amount.

John enters $250 under state and local personal property taxes. This line is for value-based taxes on movable items (like a car). A flat car registration fee would not go here. Short answer: put $250 on the personal property tax line if it is value-based.

Step 5 — Leave out flat local fees.

John does not enter the $430 for trash and stormwater. These are non-ad valorem charges tied to services, not value. He keeps the bill to show the split if asked. Short answer: skip non-ad valorem fees.

Step 6 — Quick recap with numbers.

Deductible totals: $1,214 (home ad valorem) + $250 (vehicle ad valorem) = $1,464. Not deductible: $430 in service fees. He files Schedule A with copies of the Property Tax Bill and the DMV receipt. Short answer: John deducts $1,464 and excludes $430.

Why this helps a younger filer (14–60 range).

You sort each line by one test: Is it based on value? If yes, it may go on Schedule A. If it is a flat charge, it stays off the form. Short answer: value-based in, flat fees out.

Conclusion — Simplifying the Tax Puzzle

Yes, real estate taxes sit inside property taxes, but they are not the same in how the IRS treats them. Real estate taxes hit land and buildings. Personal property taxes hit things you can move, like a car. Short answer: value-based lines can be deductible; flat service fees are not.

Here is the clean split I use at home. If the line is tied to assessed value, I tag it as ad valorem and keep it for Schedule A (Form 1040). If it is a set fee for trash, sewer, or a road project, I set it aside. Short answer: value-based in, service fees out.

States shape the bill, but the IRS rule stays the same. In Montana or Minnesota, counties set value and stack levies, yet only the value-based parts may help you at tax time. That is why I read each line, not just the total. Short answer: state sets the mix; IRS sets the deduction test.

This lens saved me from a common miss. I used to claim the whole bill and felt proud—until I saw the non-ad valorem lines. Now I only claim the parts tied to value and keep the bill as proof. Short answer: claim the ad valorem parts, keep receipts.

Take one small step today. Grab your latest property tax bill and mark the ad valorem section in pen. Do the same for any vehicle tax that is based on value. Short answer: check the ad valorem section—it is where your IRS deduction lives.

FAQ

What is the difference between property taxes and real estate taxes?

Property taxes are the big bucket. Real estate taxes are one part of that bucket for land and buildings. Only the value-based part (ad valorem) may be deductible on Schedule A, while flat service fees are not.

Did I pay property or real estate taxes?

A bill on your house or land is real estate tax. A bill on a car, RV, or boat is personal property tax. Both sit under “property taxes,” but only value-based lines may count for a deduction.

Are real estate taxes the same as property taxes on 1098?

Form 1098 shows real estate taxes your lender paid from escrow. It does not show car or other personal property taxes. Use your county bill and DMV slip to see what else you paid.

What is the difference between real estate and property?

Real estate means land and anything fixed to it. Property is a wider term that also includes movable things, like vehicles and equipment. That is why people ask if they are the same, but the rules treat them differently.

What is the difference between property taxes and real estate taxes?

Property taxes are the broad category for taxes on what you own. Real estate taxes cover only land and buildings. The IRS allows deductions only for value-based real estate taxes.

Did I pay property or real estate taxes?

If your bill is for land or a home, it’s real estate tax. If it’s for a car, RV, or boat, it’s personal property tax. Both fall under property taxes, but only value-based ones may be deductible.

Are real estate taxes the same as property taxes on 1098?

Form 1098 shows real estate taxes your lender paid from escrow. It doesn’t include vehicle or other personal property taxes. Check your county or DMV records for those amounts.

What is the difference between real estate and property?

Real estate means land and anything attached to it, like a house or garage. Property is broader and includes movable things such as vehicles or tools. The IRS treats each type differently for tax purposes.

Read More:

Business Tax Preparation in Orlando