An IRS payment plan in Orlando lets you pay federal taxes over time.

If you owe back taxes and live in Central Florida, you can still breathe easy. I help Orlando taxpayers set up the right IRS payment plan Orlando residents can use to spread payments, avoid harsh collections, and protect cash flow. This guide explains the options, steps, costs, and local tips so you can choose with confidence.

What an IRS payment plan means for Orlando taxpayers

An IRS payment plan is an agreement to pay what you owe in monthly amounts. It is also called an installment agreement. You keep filing on time. You pay on a set date each month. In most cases, the IRS stops new collection actions once your plan is active.

An IRS payment plan Orlando taxpayers use works the same as anywhere in the U.S. It is federal law. Yet local factors still matter. Florida often sees disaster relief. Orlando has a Taxpayer Assistance Center by appointment. Local tax pros also know how to keep your case smooth.

Key points to know:

- You can apply online, by mail, or with help from a pro.

- Short-term plans run up to 180 days.

- Long-term plans can last up to 72 months under streamlined rules.

- Interest and penalties still apply, but some penalties are lower on a plan.

- If you owe more, you may need to share financial data with the IRS.

→ Ready to set up your IRS payment plan in Orlando? Contact our tax relief team today for consultation and start making affordable monthly payments now.

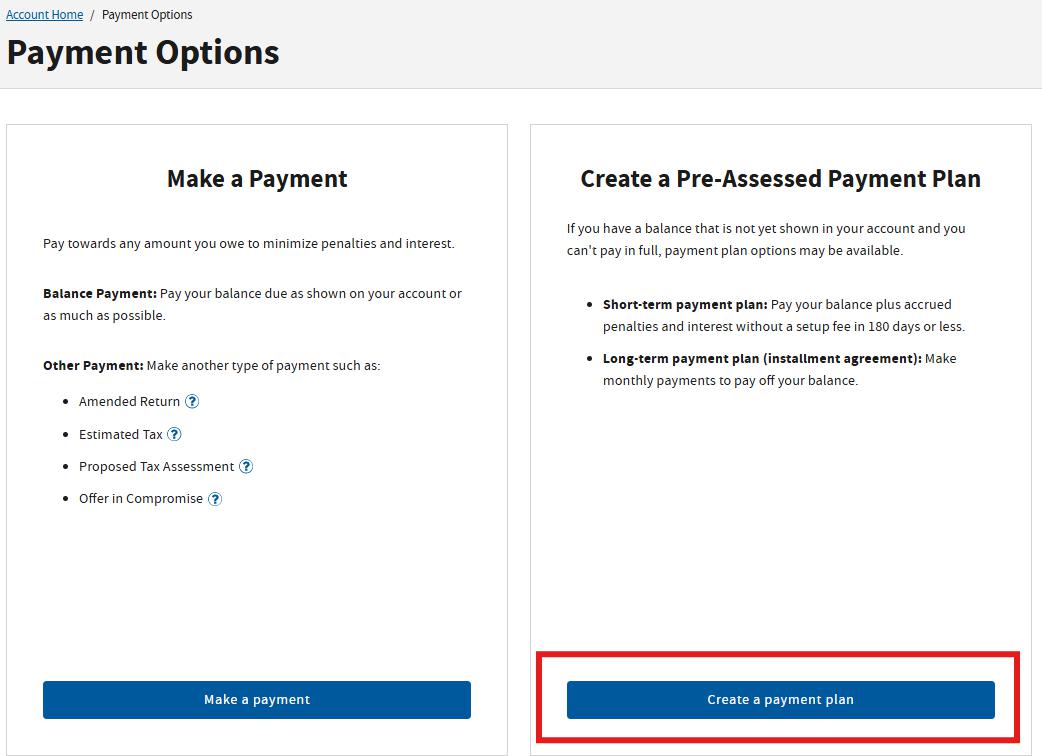

Types of IRS payment plans available from Orlando

There is no one best plan. Your balance and budget drive the choice. Here are the main options you can use when seeking an IRS payment plan Orlando solution.

Short-term payment plan (up to 180 days)

- Good if you can pay in six months.

- No setup fee.

- Interest and penalties still run until paid.

Long-term installment agreement (72 months, streamlined)

- For many individuals who owe $50,000 or less in tax, penalty, and interest.

- No detailed financial forms needed in most cases.

- Choose direct debit from your bank for best odds and fewer issues.

Direct Debit Installment Agreement (DDIA)

- Monthly auto-draft from your bank.

- Lower setup fee than other methods.

- Fewer default risks since payments are automatic.

Non-streamlined or higher-balance plans

- If you owe more than streamlined limits, the IRS may ask for financials.

- Forms can include Form 433-F or 433-A.

- The payment may track your ability to pay, not just the amount owed.

Business payment plans

- In-business trust fund express plan may work up to certain limits.

- You may need to pay within 24 months if the balance is low enough.

- Payroll tax debts need fast action to avoid hard collection moves.

Partial Payment Installment Agreement (PPIA)

- For people who cannot pay in full before the collection deadline.

- You make a lower monthly amount based on your means.

- The IRS may review your finances every two years.

Fees to expect:

- Online setup fee is often lower for direct debit plans than other methods.

- Low-income status can reduce or waive fees in some cases.

- Fees change at times. Check current IRS guidance when you apply.

Costs, penalties, and tax lien risks

With any IRS payment plan Orlando residents use, the cost includes more than the monthly amount. Know these items so there are no surprises.

- Interest accrues daily. It equals the federal short-term rate plus a margin set by law.

- The failure-to-pay penalty is usually 0.5% per month. It often drops to 0.25% per month while on a qualified installment agreement.

- A setup fee may apply. It is lower online and for direct debit. Low-income rules can reduce it.

About tax liens:

- The IRS can file a Notice of Federal Tax Lien if you owe a larger balance, often at $10,000 or more.

- A lien is public and can affect credit and property deals.

- Direct debit plans and quick action can reduce lien risks. The IRS may withdraw a lien after a set time if you qualify and keep payments current.

Default risks:

- Missed payments, new unpaid balances, or unfiled returns can cause default.

- If you default, the IRS can levy wages or accounts.

- Call fast if you hit a cash crunch. Many cases can be saved with a change or a short hold.

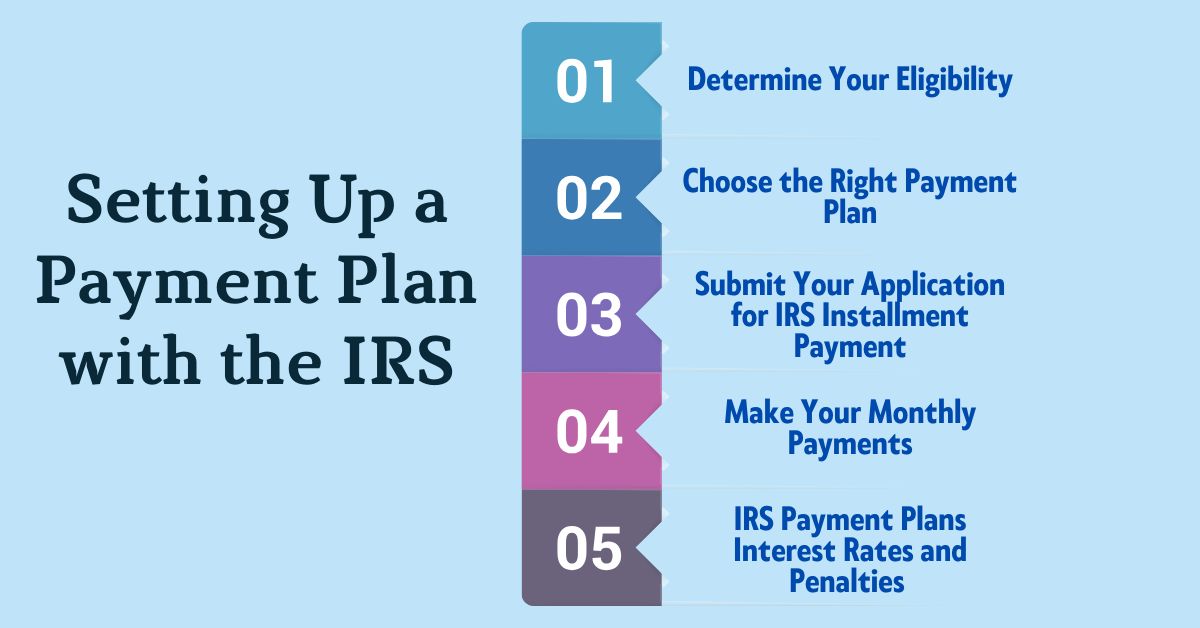

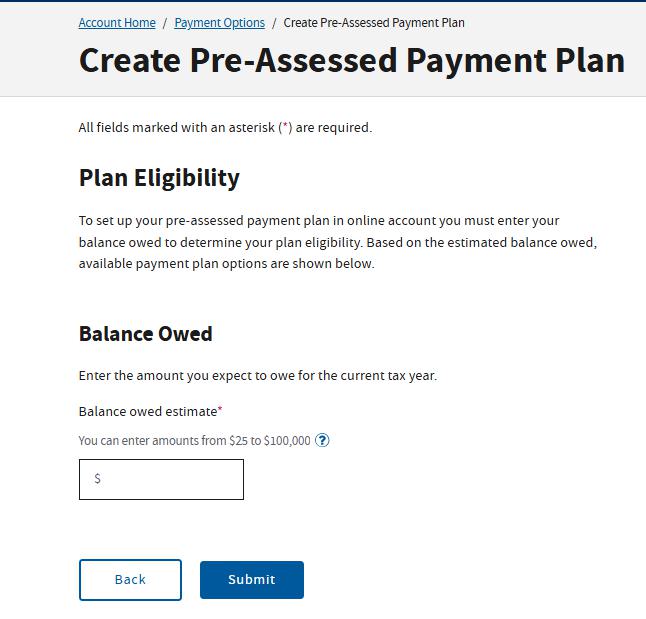

Step-by-step: Apply from Orlando

You can set up an IRS payment plan Orlando residents can trust in a few simple steps. Here is a clear path you can follow.

- Check your balance

- Create or sign in to your IRS online account.

- Confirm what you owe and the tax years involved.

- Choose your plan type

- If you can pay in six months, go short-term.

- If not, a long-term plan is better.

- Direct debit is often best. It is simpler and safer.

- Apply online when you can

- Use the Online Payment Agreement tool.

- It is fast and has the lowest setup fee in most cases.

- Use forms if needed

- Form 9465 starts a request by mail.

- If asked for financials, complete Form 433-F or 433-A.

- Be accurate and clear. This saves time.

- Make your first payment

- Set the draft date to match your cash flow.

- Use direct debit, payroll deduction (Form 2159), or another method.

- Card payments have added fees from processors.

- Keep your plan healthy

- File all returns on time.

- Adjust withholding or estimates so you do not add new debt.

- If life changes, call the IRS or your pro and adjust the plan.

Local help:

- The Orlando Taxpayer Assistance Center meets by appointment. Call 844-545-5640 to book.

- A local enrolled agent or CPA can also help set terms and fix snags.

Orlando-specific tips and local help

An IRS payment plan Orlando fit should reflect local life. Here are notes from working with Central Florida clients.

- Florida has no state income tax. Your focus is the IRS balance and cash flow.

- Storms happen. When the IRS grants disaster relief, you may get more time. Check the IRS disaster page for Florida updates.

- Tourism and gig work can mean uneven income. Pick a draft date that follows your best cash week.

- Use a separate savings account for taxes. Transfer weekly if your pay is variable. This habit changes everything.

Personal tips I share with clients:

- Keep the payment date close to payday. Missed drafts cause chaos.

- If you owe more than you can handle, ask about a PPIA or an Offer in Compromise.

- Save every letter. Call as soon as you get a notice you do not understand.

- When in doubt, ask a local pro. A 30-minute review can prevent months of stress.

If a payment plan is not enough

Sometimes an IRS payment plan Orlando residents consider is not the right move. These options can help when cash is tight.

- Offer in Compromise

You settle for less than you owe if you qualify. The IRS checks your income, assets, and expenses. It is slow but can be life-changing. - Currently Not Collectible (CNC)

The IRS pauses collection if you cannot pay basic bills. Interest and penalties continue. You must update the IRS if asked. - Penalty relief

First-time abatement or reasonable cause can lower penalties. You still pay tax and interest. Apply early to cut total cost. - Amend or fix returns

If a return is wrong, fix it. The true balance could be lower. This is the cleanest way to reduce pain fast. - Adjust withholding or estimates

Stop new balances from forming. Raise your W-4 withholding or make quarterly payments on time.

Real-life Orlando examples and lessons

Here are short, real cases from my work with Orlando taxpayers. Names and details are changed, but the lessons are true.

- The rideshare pro

She owed $18,400 after a tough year. We set a direct debit plan at a number she could keep. We also raised her quarterly estimates. She stayed current and avoided a lien. - The family shop owner

Payroll taxes fell behind. We set a business plan and a tight budget. We filed all late returns fast. He paid on time and kept his doors open. - The nurse who moved from out of state

She missed a 1099. We amended a return and cut the balance by 30%. Then we used a short-term plan and cleared the rest within five months.

Lessons learned:

- File first. Then pay. The IRS wants returns on time.

- Pick a realistic amount. A smaller, steady plan beats a big plan you miss.

- Automate. Direct debit prevents slips.

- Talk early if money gets tight. Options shrink if you wait.

Quick answers to common search questions

Can I get an IRS payment plan if I live in Orlando?

Yes. An IRS payment plan Orlando residents use is the same federal program. You can apply online or with help from a local pro.

How long does IRS approval take?

Online plans can be approved right away. Mail-in plans or those with financial forms can take weeks.

Does a plan stop IRS collections?

Once a plan is active, new levies usually stop. You must keep payments and filings current to stay protected.

Frequently Asked Questions of IRS payment plan Orlando

What credit score do I need for an IRS payment plan?

The IRS does not use your credit score to approve a plan. They look at your balance, filings, and your ability to pay.

Will an IRS payment plan affect my credit in Orlando?

The plan itself is not reported to credit bureaus. A filed federal tax lien can affect credit and public records.

Can I choose the payment date and amount?

Yes, within reason. Pick a date that matches your cash flow and an amount that you can sustain.

What happens if I miss a payment?

You may get a default notice. Call fast to make it right or adjust the plan before harsher steps start.

Can I include multiple tax years in one plan?

Yes. Most plans cover all open balances. You must keep future returns and payments on time.

Are setup fees different if I apply online?

Often, yes. Online direct debit plans usually have lower setup fees. Low-income rules can reduce or waive fees.

Can a tax pro set up the plan for me?

Yes. A CPA, enrolled agent, or attorney can act for you. They can also help you pick the best plan and avoid errors.

Conclusion

An IRS payment plan Orlando taxpayers can rely on is within reach. Choose the plan that fits your budget, automate drafts, and file on time. Add smart moves like better withholding, clean records, and fast replies to notices.

Take the next step today. Check your IRS balance, pick your plan, and set your first draft date. If you want help, talk with a trusted local pro. Share your questions or stories below, and subscribe for more clear tax tips you can use.

Read More:

→ IRS Tax Problem Solvers

→ Can You Go to Jail for Not Paying Taxes